Page 9 - Profmark Tax Guide 2025

P. 9

Employees’ tax is based on 80% of the travel allowance� However, if the

employer is satisfied that at least 80% of the use of a motor vehicle will be

for business purposes, employees’ tax may be based on 20% of the travel

allowance�

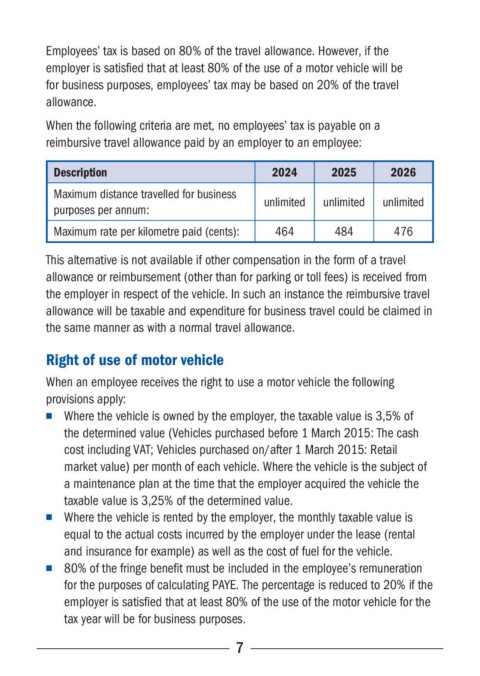

When the following criteria are met, no employees’ tax is payable on a

reimbursive travel allowance paid by an employer to an employee:

Description 2024 2025 2026

Maximum distance travelled for business unlimited unlimited unlimited

purposes per annum:

Maximum rate per kilometre paid (cents): 464 484 476

This alternative is not available if other compensation in the form of a travel

allowance or reimbursement (other than for parking or toll fees) is received from

the employer in respect of the vehicle� In such an instance the reimbursive travel

allowance will be taxable and expenditure for business travel could be claimed in

the same manner as with a normal travel allowance�

Right of use of motor vehicle

When an employee receives the right to use a motor vehicle the following

provisions apply:

■ Where the vehicle is owned by the employer, the taxable value is 3,5% of

the determined value (Vehicles purchased before 1 March 2015: The cash

cost including VAT; Vehicles purchased on/after 1 March 2015: Retail

market value) per month of each vehicle� Where the vehicle is the subject of

a maintenance plan at the time that the employer acquired the vehicle the

taxable value is 3,25% of the determined value�

■ Where the vehicle is rented by the employer, the monthly taxable value is

equal to the actual costs incurred by the employer under the lease (rental

and insurance for example) as well as the cost of fuel for the vehicle�

■ 80% of the fringe benefit must be included in the employee’s remuneration

for the purposes of calculating PAYE� The percentage is reduced to 20% if the

employer is satisfied that at least 80% of the use of the motor vehicle for the

tax year will be for business purposes�

7