Page 10 - Profmark Tax Guide 2025

P. 10

■ On assessment the fringe benefit for the tax year is reduced by the ratio of

the distance travelled for business purposes substantiated by a log book

divided by the actual distance travelled during the tax year�

■ On assessment further relief is available for the cost of licence, insurance,

maintenance and fuel for private travel if the full cost thereof has been

borne by the employee and if the distance travelled for private purposes is

substantiated by a log book�

Subsistence allowances and advances

Where an advance or allowance is received by an employee for meals and other

incidental costs, he / she can deduct either:

■ The amount actually spent (limited to the advance or allowance), or

■ For a day trip where employee is not spending at least one night away from

his/her normal place of residence, an amount not exceeding R176�

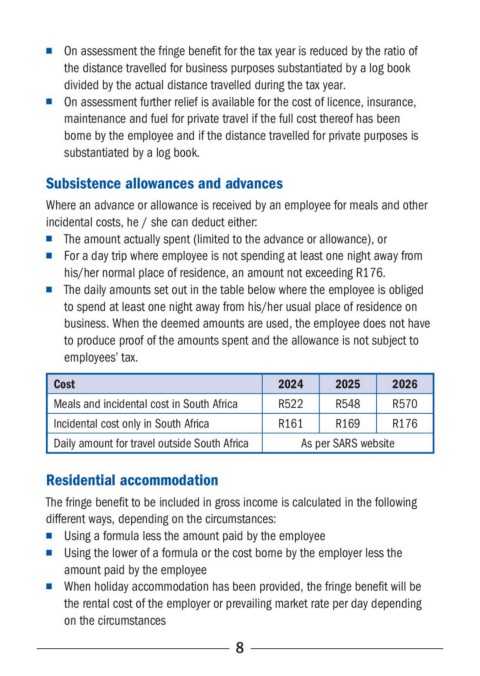

■ The daily amounts set out in the table below where the employee is obliged

to spend at least one night away from his/her usual place of residence on

business� When the deemed amounts are used, the employee does not have

to produce proof of the amounts spent and the allowance is not subject to

employees’ tax�

Cost 2024 2025 2026

Meals and incidental cost in South Africa R522 R548 R570

Incidental cost only in South Africa R161 R169 R176

Daily amount for travel outside South Africa As per SARS website

Residential accommodation

The fringe benefit to be included in gross income is calculated in the following

different ways, depending on the circumstances:

■ Using a formula less the amount paid by the employee

■ Using the lower of a formula or the cost borne by the employer less the

amount paid by the employee

■ When holiday accommodation has been provided, the fringe benefit will be

the rental cost of the employer or prevailing market rate per day depending

on the circumstances

8