Page 56 - Profmark Tax Guide 2025

P. 56

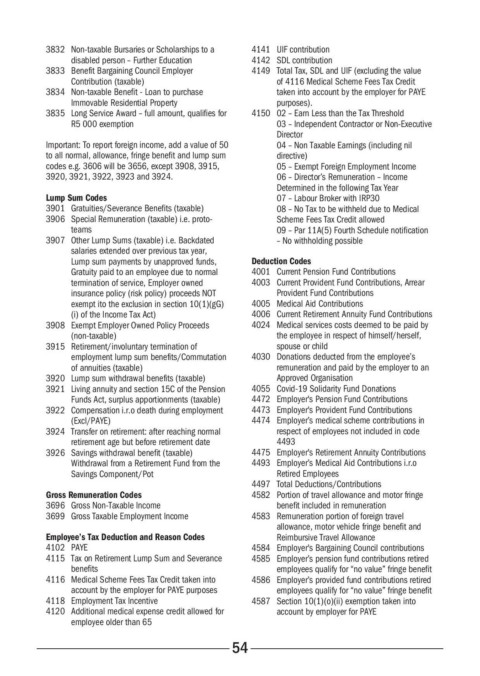

3832 Non-taxable Bursaries or Scholarships to a 4141 UIF contribution

disabled person – Further Education 4142 SDL contribution

3833 Benefit Bargaining Council Employer 4149 Total Tax, SDL and UIF (excluding the value

Contribution (taxable) of 4116 Medical Scheme Fees Tax Credit

3834 Non-taxable Benefit - Loan to purchase taken into account by the employer for PAYE

Immovable Residential Property purposes)�

3835 Long Service Award – full amount, qualifies for 4150 02 – Earn Less than the Tax Threshold

R5 000 exemption 03 – Independent Contractor or Non-Executive

Director

Important: To report foreign income, add a value of 50 04 – Non Taxable Earnings (including nil

to all normal, allowance, fringe benefit and lump sum directive)

codes e�g� 3606 will be 3656, except 3908, 3915, 05 – Exempt Foreign Employment Income

3920, 3921, 3922, 3923 and 3924� 06 – Director’s Remuneration – Income

Determined in the following Tax Year

Lump Sum Codes 07 – Labour Broker with IRP30

3901 Gratuities/Severance Benefits (taxable) 08 – No Tax to be withheld due to Medical

3906 Special Remuneration (taxable) i�e� proto- Scheme Fees Tax Credit allowed

teams 09 – Par 11A(5) Fourth Schedule notification

3907 Other Lump Sums (taxable) i�e� Backdated – No withholding possible

salaries extended over previous tax year,

Lump sum payments by unapproved funds, Deduction Codes

Gratuity paid to an employee due to normal 4001 Current Pension Fund Contributions

termination of service, Employer owned 4003 Current Provident Fund Contributions, Arrear

insurance policy (risk policy) proceeds NOT Provident Fund Contributions

exempt ito the exclusion in section 10(1)(gG) 4005 Medical Aid Contributions

(i) of the Income Tax Act) 4006 Current Retirement Annuity Fund Contributions

3908 Exempt Employer Owned Policy Proceeds 4024 Medical services costs deemed to be paid by

(non-taxable) the employee in respect of himself/herself,

3915 Retirement/involuntary termination of spouse or child

employment lump sum benefits/Commutation 4030 Donations deducted from the employee’s

of annuities (taxable) remuneration and paid by the employer to an

3920 Lump sum withdrawal benefits (taxable) Approved Organisation

3921 Living annuity and section 15C of the Pension 4055 Covid-19 Solidarity Fund Donations

Funds Act, surplus apportionments (taxable) 4472 Employer's Pension Fund Contributions

3922 Compensation i�r�o death during employment 4473 Employer's Provident Fund Contributions

(Excl/PAYE) 4474 Employer’s medical scheme contributions in

3924 Transfer on retirement: after reaching normal respect of employees not included in code

retirement age but before retirement date 4493

3926 Savings withdrawal benefit (taxable) 4475 Employer's Retirement Annuity Contributions

Withdrawal from a Retirement Fund from the 4493 Employer’s Medical Aid Contributions i�r�o

Savings Component /Pot Retired Employees

4497 Total Deductions/Contributions

Gross Remuneration Codes 4582 Portion of travel allowance and motor fringe

3696 Gross Non-Taxable Income benefit included in remuneration

3699 Gross Taxable Employment Income 4583 Remuneration portion of foreign travel

allowance, motor vehicle fringe benefit and

Employee’s Tax Deduction and Reason Codes Reimbursive Travel Allowance

4102 PAYE 4584 Employer's Bargaining Council contributions

4115 Tax on Retirement Lump Sum and Severance 4585 Employer’s pension fund contributions retired

benefits employees qualify for “no value” fringe benefit

4116 Medical Scheme Fees Tax Credit taken into 4586 Employer’s provided fund contributions retired

account by the employer for PAYE purposes employees qualify for “no value” fringe benefit

4118 Employment Tax Incentive 4587 Section 10(1)(o)(ii) exemption taken into

4120 Additional medical expense credit allowed for account by employer for PAYE

employee older than 65

54