Page 37 - Profmark BSA Guide 2025

P. 37

Transfer Duty

■ Calculated on the value of immovable property

■ Payable within six months after the transaction is entered into

■ Exemptions apply with the most notable when the seller is a VAT vendor

■ Where a VAT vendor purchases property from a non-vendor, the notional input

tax is calculated by multiplying the tax fraction (15/115) by the lesser of the

consideration paid or market value

■ The acquisition of a contingent right in a trust that holds a residential property or

the shares in a company or the member’s interest in a close corporation, which

owns residential property, comprising more than 50% of its assets, is subject to

transfer duty at the applicable rate

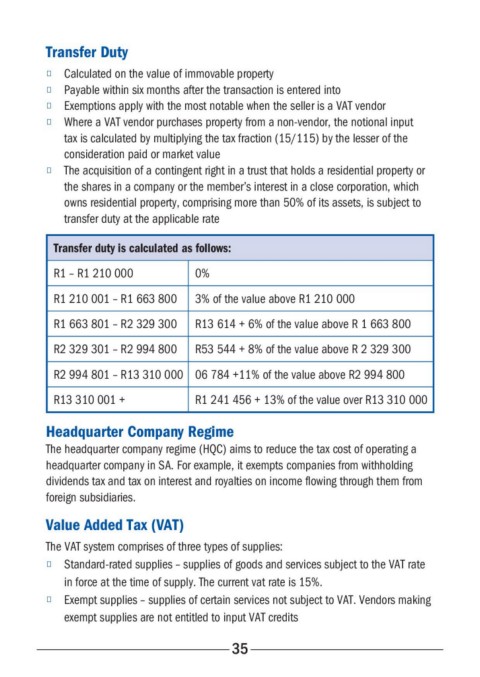

Transfer duty is calculated as follows:

R1 – R1 210 000 0%

R1 210 001 – R1 663 800 3% of the value above R1 210 000

R1 663 801 – R2 329 300 R13 614 + 6% of the value above R 1 663 800

R2 329 301 – R2 994 800 R53 544 + 8% of the value above R 2 329 300

R2 994 801 – R13 310 000 06 784 +11% of the value above R2 994 800

R13 310 001 + R1 241 456 + 13% of the value over R13 310 000

Headquarter Company Regime

The headquarter company regime (HQC) aims to reduce the tax cost of operating a

headquarter company in SA. For example, it exempts companies from withholding

dividends tax and tax on interest and royalties on income flowing through them from

foreign subsidiaries.

Value Added Tax (VAT)

The VAT system comprises of three types of supplies:

■ Standard-rated supplies – supplies of goods and services subject to the VAT rate

in force at the time of supply. The current vat rate is 15%.

■ Exempt supplies – supplies of certain services not subject to VAT. Vendors making

exempt supplies are not entitled to input VAT credits

35