Page 32 - Profmark Tax Guide 2025

P. 32

VALUE-ADDED TAX (VAT)

The VAT system comprises of three types of supplies:

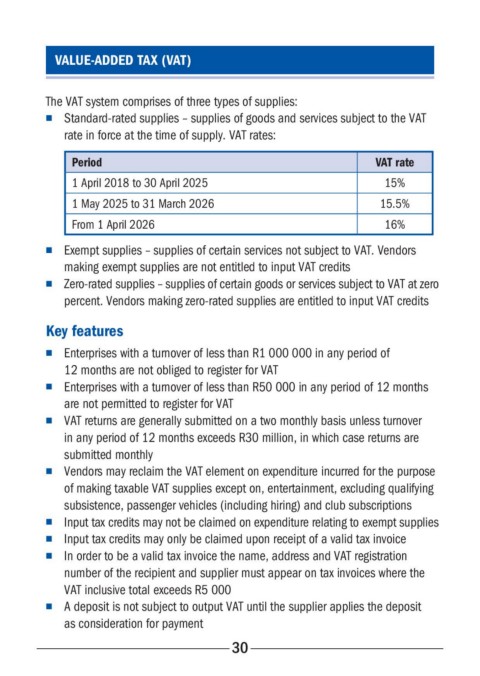

■ Standard-rated supplies – supplies of goods and services subject to the VAT

rate in force at the time of supply. The current vat rate is 15%.

■ Exempt supplies – supplies of certain services not subject to VAT. Vendors

making exempt supplies are not entitled to input VAT credits

■ Zero-rated supplies – supplies of certain goods or services subject to VAT at

zero percent. Vendors making zero-rated supplies are entitled to input VAT

credits

Key features

■ Enterprises with a turnover of less than R1 000 000 in any period of

12 months are not obliged to register for VAT

■ Enterprises with a turnover of less than R50 000 in any period of 12 months

are not permitted to register for VAT

■ VAT returns are generally submitted on a two monthly basis unless turnover

in any period of 12 months exceeds R30 million, in which case returns are

submitted monthly

■ Vendors may reclaim the VAT element on expenditure incurred for the

purpose of making taxable VAT supplies except on, entertainment, excluding

qualifying subsistence, passenger vehicles (including hiring) and club

subscriptions

■ Input tax credits may not be claimed on expenditure relating to exempt

supplies

■ Input tax credits may only be claimed upon receipt of a valid tax invoice

■ In order to be a valid tax invoice the name, address and VAT registration

number of the recipient and supplier must appear on tax invoices where the

VAT inclusive total exceeds R5 000

■ A deposit is not subject to output VAT until the supplier applies the deposit

as consideration for payment

30