Page 65 - Profmark_2024_Directors Guide

P. 65

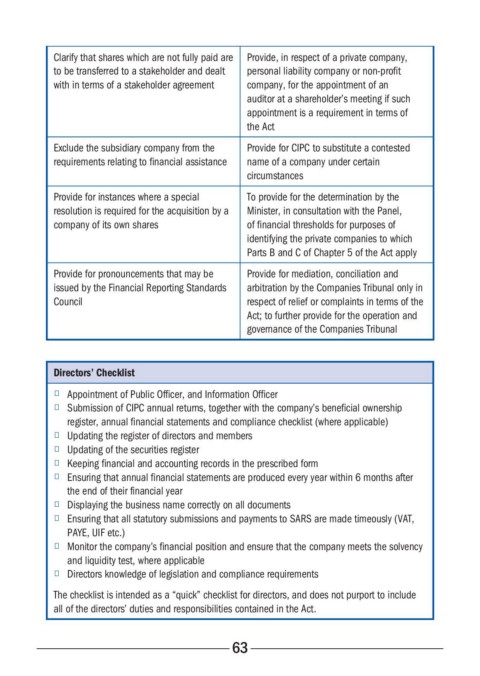

Clarify that shares which are not fully paid are Provide, in respect of a private company,

to be transferred to a stakeholder and dealt personal liability company or non-profit

with in terms of a stakeholder agreement company, for the appointment of an

auditor at a shareholder’s meeting if such

appointment is a requirement in terms of

the Act

Exclude the subsidiary company from the Provide for CIPC to substitute a contested

requirements relating to financial assistance name of a company under certain

circumstances

Provide for instances where a special To provide for the determination by the

resolution is required for the acquisition by a Minister, in consultation with the Panel,

company of its own shares of financial thresholds for purposes of

identifying the private companies to which

Parts B and C of Chapter 5 of the Act apply

Provide for pronouncements that may be Provide for mediation, conciliation and

issued by the Financial Reporting Standards arbitration by the Companies Tribunal only in

Council respect of relief or complaints in terms of the

Act; to further provide for the operation and

governance of the Companies Tribunal

Directors’ Checklist

■ Appointment of Public Officer, and Information Officer

■ Submission of CIPC annual returns, together with the company’s beneficial ownership

register, annual financial statements and compliance checklist (where applicable)

■ Updating the register of directors and members

■ Updating of the securities register

■ Keeping financial and accounting records in the prescribed form

■ Ensuring that annual financial statements are produced every year within 6 months after

the end of their financial year

■ Displaying the business name correctly on all documents

■ Ensuring that all statutory submissions and payments to SARS are made timeously (VAT,

PAYE, UIF etc.)

■ Monitor the company’s financial position and ensure that the company meets the solvency

and liquidity test, where applicable

■ Directors knowledge of legislation and compliance requirements

The checklist is intended as a “quick” checklist for directors, and does not purport to include

all of the directors’ duties and responsibilities contained in the Act.

63