Page 58 - Profmark BSA Guide 2025

P. 58

Dismissal

The LRA grants employees protection against unfair dismissal. A dismissal must

be both substantively and procedurally fair. The three main grounds for dismissal

are misconduct, incapacity (ill health or poor work performance) and operational

requirements of the employer. Payment on dismissal includes accrued annual leave pay,

payment in lieu of notice – unless summarily dismissed or if the employee is required

to work the notice period. If dismissal is due to operational requirements, severance

pay of a minimum of one week’s salary for every completed year of service, and any

other amount that the employee is contractually entitled to.

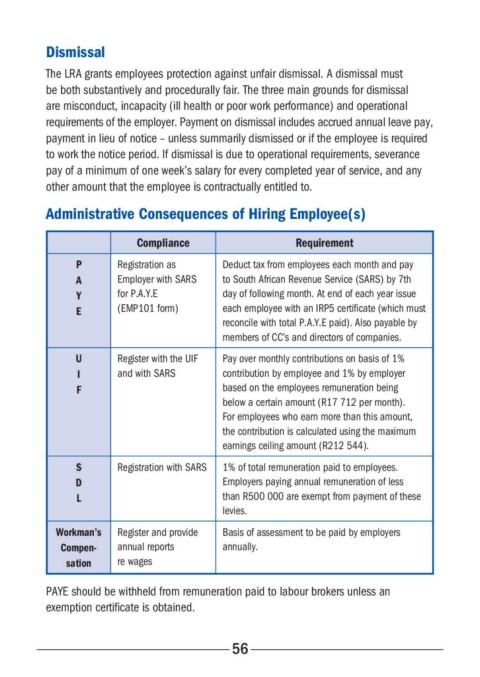

Administrative Consequences of Hiring Employee(s)

Compliance Requirement

P Registration as Deduct tax from employees each month and pay

A Employer with SARS to South African Revenue Service (SARS) by 7th

Y for P.A.Y.E day of following month. At end of each year issue

E (EMP101 form) each employee with an IRP5 certificate (which must

reconcile with total P.A.Y.E paid). Also payable by

members of CC’s and directors of companies.

U Register with the UIF Pay over monthly contributions on basis of 1%

I and with SARS contribution by employee and 1% by employer

F based on the employees remuneration being

below a certain amount (R17 712 per month).

For employees who earn more than this amount,

the contribution is calculated using the maximum

earnings ceiling amount (R212 544).

S Registration with SARS 1% of total remuneration paid to employees.

D Employers paying annual remuneration of less

L than R500 000 are exempt from payment of these

levies.

Workman’s Register and provide Basis of assessment to be paid by employers

Compen- annual reports annually.

sation re wages

PAYE should be withheld from remuneration paid to labour brokers unless an

exemption certificate is obtained.

56